What I Do With My Money

Keepin’ it easy, breezy, Cover Girl

Way Back Playback: Recap

Hello, friends! I noticed that a few warm bodies (or bots) have joined the substack - welcome all! As we forge into the unknown together, I thought it would be helpful to recap what I’ve shared thus far:

My lofty declaration to save 50% of my net income this year (the world, or roughly 52 people, is watching)

How I figured out where my money is going (and how you can too)

How I now think of money (keep your emissaries moving, folks!)

This week is all about what *I* do with *MY* sweaty, meaty cash. Before I dive into the details as I’m learning them, I want to offer a disclaimer: what I’m about to share is not investment advice. What I outline below are tactics that I’m comfortable with testing. Everyone’s financial situation is different. What works for me, may not work for you. With anything, if you see something that intrigues you, research, learn more and figure out what will work best for you based on your preferences, risk tolerances and life. Now that's out of the way, let’s dive in!

Coaches In Unlikely Places

Growing up, no one gives you a how-to guide for handling your finances. Sure, in school they teach you “math,” but I don’t recall learning anything about how to handle money. Even if such information was offered to a snot nosed teenager, I doubt I would remember - not when Dawson’s Creek captured the imagination of my generation. No, I was not attuned to such life altering knowledge as a pimple faced 15 year old.

Now, however, is different. Now I’m ready. Now I have adult acne.

But knowing you’re ready to accept life altering knowledge and actually gaining access to that knowledge are two very different things. I always thought that once you’re ready to accept the universe’s wisdom, the universe would send you a Mr. Miyagi or Ted Lasso or Michelle Obama to teach you. Turns out, not the case.

Turns out in real-life we need to seek out resources and get a little creative with the form potential coaches can take. Realizing this, I started to look in different places and spaces for financial coaches and resources. Enter stage right: the most sane and intelligent digital platform that ever existed, Instagram.

The Day I Met Jack

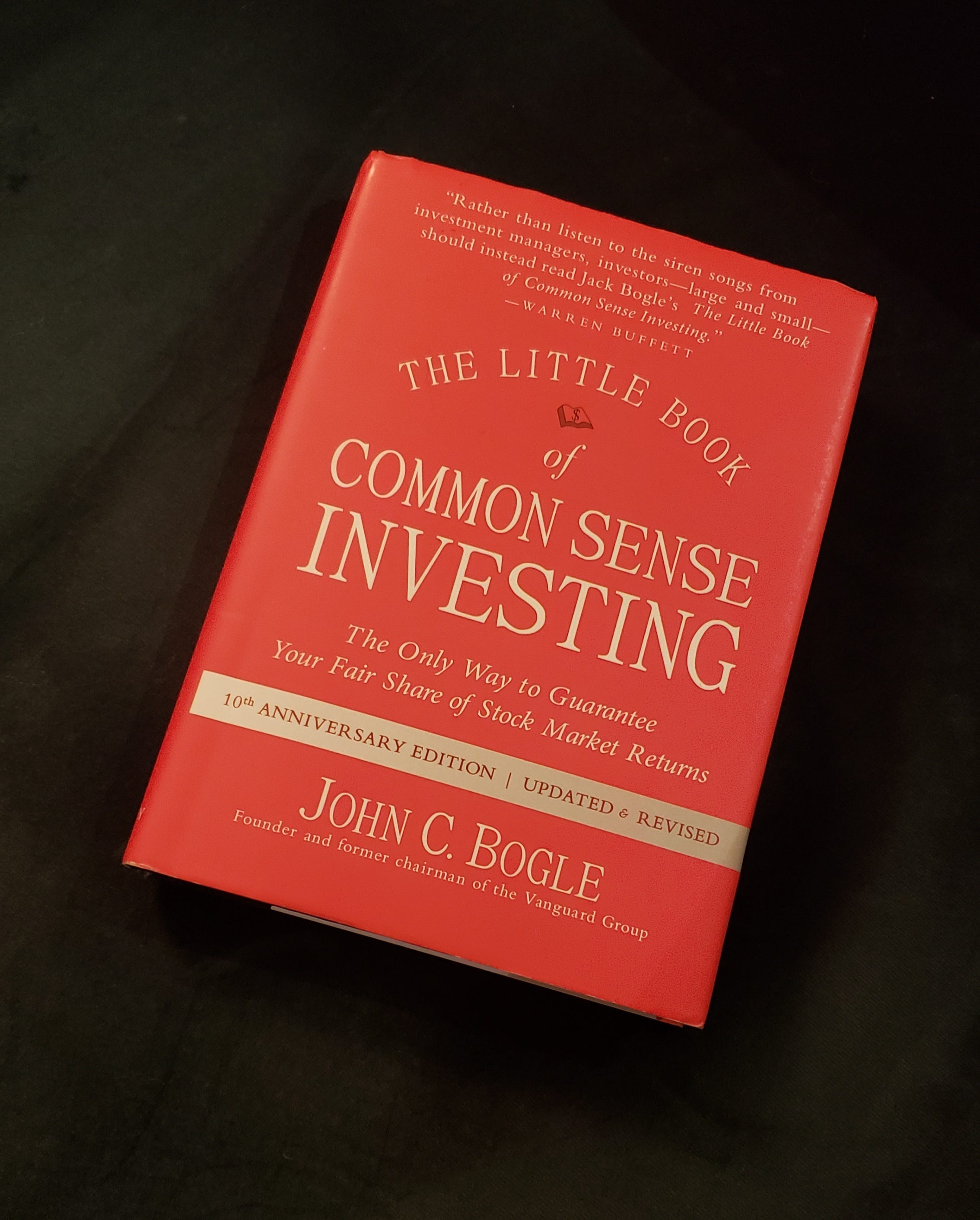

There I was, mindlessly consuming content about god knows what on Instagram when the algorithm fed me a tasty treat in the form of content about investing. An image of a book popped up on my screen:

For whatever reason the red book jacket twinkled in my eye and I flicked my thumb, opened my Amazon app and purchased what my subconscious assumed was yet another book I would never read. (Collecting books I never read is one of my favourite hobbies. Some people collect spoons, I collect books.)

When the book arrived I was surprised by it, it's in fact quite small. As I flipped through the pages, the content looked oddly accessible. I read a chapter, and then another, and another. I became hooked. In the end, it was a complete game changer for me.

To offer a brief summary of The Little Book of Common Sense Investing: the book explains how the stock market works, how stocks work, and how to ignore the noise of these two things and select a conservative but winning investment strategy.

The author, John C. Bogle, or Jack to his friends, was essentially a punk. As a recovering academic, he worked on Wall Street long enough to collect a wealth of practical knowledge and piss off his employer enough to get himself fired. From there, he went on to found one of the most profitable investment companies solely dedicated to NOT screwing over clients. An anomaly for investment management firms, his company actually prioritizes customers’ investment growth over maximizing company profits. His firm did this by creating stable, relatively low risk diversified index funds offered at rock bottom prices to customers (among many other things). The little company he created is called The Vanguard Group, which now manages about $7.7 trillion (USD) in global assets.

If you are interested in maximizing your investments, I HIGHLY RECOMMEND you read this book. It’s a MUST read for anyone unsure of how to get their money working for them (or how to keep it moving).

What I Do With My Sweaty, Meaty, Slimy Cash

It took me a little while to figure out exactly what I wanted to do with my money. There is A LOT of noise out there about saving and investing. People from all walks of life seem to hold secrets to unlocking unparalleled financial returns, shouting: “You need to buy this stock now!” or “You need to buy real estate now!” (laughable advice for Canadians who don’t already own real estate). I was pretty overwhelmed and confused initially.

But after meeting Jack, who preaches simplicity and low cost above all, the fog of confusion started to lift. Though initially cautious of investing in the stock market, the tactics Jack lays out in his book seemed foolish not to at least try. Which is essentially this: buy a diversified index fund with rock bottom management fees and hold it until you die.

Sounds simple enough! #dying

The Breakdown

It’s important to note that as a newly minted investor at the age of (deep breath) 39, I am focused on keeping my money (or emissaries) as active as possible. For me, this means growth, which translates to investing in stocks. This is what I do:

Of the income I save per month I invest 40% into a RRSP, I invest another 40% into a TFSA, and the final 20% into an emergency fund.

My RRSP and TFSA hold the same stock: VFV (the Canadian equivalent of the American Vanguard S&P 500 Index ETF).

My emergency fund is in a high-interest savings account that earns me 4.5% interest, compounded monthly.

I also have a contribution matching RRSP with my employer. I take full advantage of this, contributing the maximum amount the company will match. This investment is held in a growth retirement index fund.

And that’s it. It’s that simple. I’m a basic b*tch investor.

Now, with this oh-so-simple strategy, you may be thinking: “this girl is nuts! Only holding one stock?? If that stock tanks, she will be poor AF.” While technically true, I highly doubt that will happen. The reason being, this fund is naturally diversified. The S&P 500 Index tracks the top 500 companies in the US across all sectors (aka with one fund you own a small amount of each of the top 500 companies in the US). So, unless the US economy completely tanks (which, I would argue, would lead to MUCH BIGGER concerns than anything to do with investments), it’s a sound investment strategy (for me).

Some Initial Mistakes, Whoopsies!

When I first transferred my investments over to Wealthsimple (a Canadian based investment and banking app), I tried to be cute and invested in a variety of index funds (there are thousands out there), thinking they’re all essentially the same. I quickly learned they are not.

Keeping a bunch of index funds on the books, my return was alright, around 5-6% throughout the first three months. But then I started digging into the cost of the funds and I did not like what I found. Foolishly, I did not heed Jack’s advice wholeheartedly from the beginning.

Index funds are great because they’re diversified, however, their fee structures are as varied as the amount of stocks they can potentially hold. For example, one fund I carried had a management fee of over 2%, which is bananas. In comparison, VFV has a management fee of 0.09%.

After these initial three months of donating far too much of my money to management fees, I moved all of my sweaty (so sweaty) cash into VFV. Since then, I’ve seen a 12.32% return in the last quarter. Having transferred my investments in July 2023, I’ve seen a 8.65% all-time return. Not bad.

Could I be making larger returns? Sure. Could I be swimming in pools of disgusting, sweaty cash? Maybe. At the end of the day, keeping it simple is paramount for me. I’m at the beginning of my investment journey, simple is best until I learn more. Though I made a few mistakes initially, switching over to VFV simplified a lot of things. I acknowledge that the healthy returns I’ve seen so far will likely change going forward. They might grow, they might shrink, but that’s a risk I’m willing take and I’m comfortable with that.

There is SO MUCH MORE to say on the topics of investing and diversifying further (boring bonds have their time and place too). I’ll share more as I continue to learn in the coming weeks and months.

For now, I’ll leave it there and let you enjoy this photo of my cat, Misty:

Remember, we’ve got this!

REQUEST: If you’ve been enjoying my content, I would love to hear from you. Do you have any questions about topics I’ve shared so far or are there topics you’d like me to explore in more detail? If so, please leave questions, ideas or thoughts in the comments. I want to make this substack experience fun for everyone!

TEASER: I have plans to create and regularly update a resources post, and breakdown what tools I use to invest, which are shockingly simple.

Hey, good job on investing in Index funds! I've been in VEQT for a few years now. As long as you don't panic and sell during a drop, you can expect to get decent returns. I would suggest possibly diversifying a bit. Since VFV is only the S&P500, diversifying globally in something like VEQT/XEQT might be a better choice. Or for someone with a lower risk tolerance, VGRO or VBAL are great choices too. Ben Felix has some great evidence based videos on this

https://youtu.be/RR7e1Y-HJxQ?si=8U4Fp0XLDSsW9grl